14.12°C Kathmandu

14.12°C Kathmandu

Thu, Mar 26, 2026

Money

Drop in loanable fund prompts banks to raise deposit rates

Commercial banks have once again started collecting deposits at higher interest rates, as the stock of funds that could be immediately disbursed as loans has started shrinking.

bookmark

Published at : November 30, 2017

Updated at : November 30, 2017 08:51

Kathmandu

Commercial banks have once again started collecting deposits at higher interest rates, as the stock of funds that could be immediately disbursed as loans has started shrinking.

Siddhartha Bank, on Wednesday, issued a public notice to provide return of 8 percent per annum on savings deposit. Other banks have also started raising interest on both savings and fixed deposit to attract depositors.

Around this time in the last fiscal year, banks had aggressively raised deposit rates, as they faced shortage of loanable funds due to mismatch in deposit collection and credit disbursement. Considering the present scenario, the possibility of a replay of events of last fiscal year cannot be ruled out, because credit disbursement has accelerated since the beginning of the current fiscal year in mid-July while deposit growth has slowed.

“Lending has jumped in the current fiscal year because there was backlog from the last fiscal year when many banks couldn’t meet borrowers’ demand due to shortage of loanable funds,” Mega Bank CEO Anil Shah said.

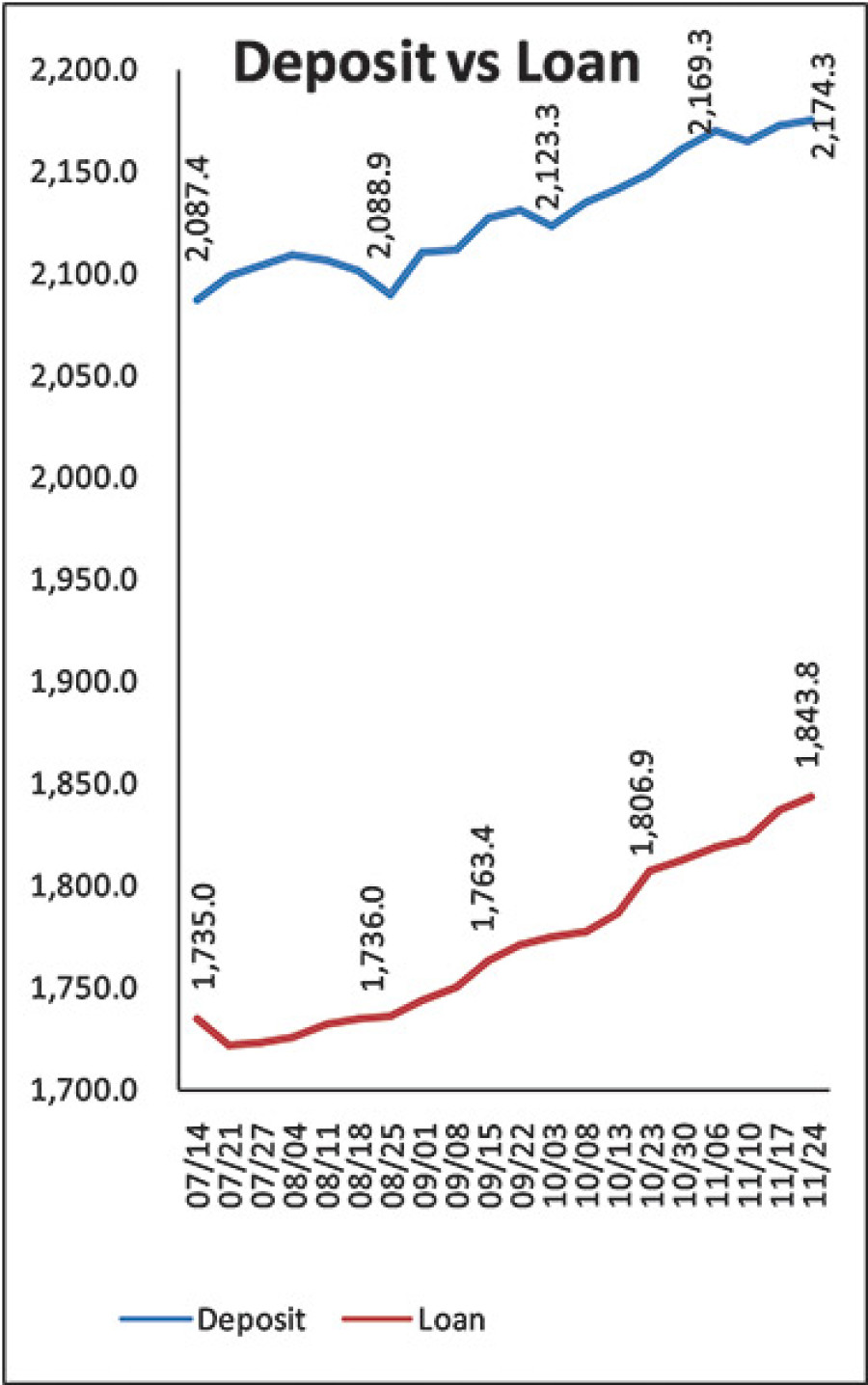

Credit disbursement of commercial banks stood at around Rs109 billion in between July 14 and November 24, show the latest data of the Nepal Bankers’ Association (NBA), the umbrella body of commercial banks. On the other hand, deposit collection hovered around Rs75 billion in the same period. Commercial banks had disbursed Rs119 billion in loan and collected Rs93 billion in deposit in the same period of the last fiscal year.

These data show that gap in deposit collection and credit disbursement has widened over the months. So far this fiscal year, banks have extended Rs1.4 in loan for every rupee of deposit raised. Banks had disbursed Rs1.3 in credit for every rupee of deposit collected in the same period of the last fiscal year.

“We are aware that the mismatch in deposit collection and credit disbursement has tightened liquidity position of banks. But we don’t think the banking sector will face acute shortage of funds that could be immediately extended as loans as in the last fiscal year because spending has gone up in the run up to federal parliamentary and provincial assembly elections. Also, the government has recently released around Rs75 billion to local bodies. We think these funds will gradually enter the banking system,” Shah said.

Banks were sitting atop loanable fund of around Rs88 billion as of November 24, NBA data show. This marks a drop of around 15 percent from a month ago when loanable fund of commercial banks hovered around Rs104 billion.

The problem facing banks at the moment is slow growth in deposit collection. This is largely the result of deceleration in remittance inflow. Nepal’s remittance income rose by mere 2.6 percent to Rs176.3 billion in the first quarter of the current fiscal year. Remittance inflow had gone up by 3.2 percent in the same period of the last fiscal year.

“Deceleration in remittance inflow coupled with low capital spending has hit deposit collection of banks,” Sanima Bank CEO Bhuvan Dahal said.

The Nepal Rastra Bank (NRB), the central bank, has said it is closely monitoring the situation. “We will use instruments at our disposal whenever there is need,” NRB Spokesperson Narayan Prasad Paudel said. “But so far it appears only a handful of banks are facing shortage of loanable funds.”

Most Read from Money

Nepal risks losing up to 132,000 jobs, $1 billion after LDC exit

Kathmandu frets over cooking gas, but oil corporation says supply normal

Global oil shock tests Nepal, but electric cooking cushions blow

Nepal’s 17 pride projects may take 41 years to finish, warns World Bank

Third graft case filed over China-funded Pokhara airport, 21 charged

Editor's Picks

Nepal risks losing up to 132,000 jobs, $1 billion after LDC exit

Raped and left to die, teenager’s family wants answers

Bengal tigers move to mid-hills. Sighted in Palpa, Arghakhanchi

Escaping poverty at home, Nepali women fall into the Gulf trap

Once the heartbeat of Nepali democracy, now a ghostly shell

E-PAPER | March 26, 2026

×