21.07°C Kathmandu

21.07°C Kathmandu

Wed, Aug 5, 2026

Columns

Why Nepal's economic future is now tethered to the stock market

Driven by an unprecedented surge to 7.9 million accounts, Nepal’s stock market has transformed from a peripheral playground into a massive economic force now equivalent to 72 percent of the country’s GDP..png&w=900&height=601)

bookmark![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

Adarsha Bazgain

Published at : June 17, 2026

Updated at : June 17, 2026 18:48

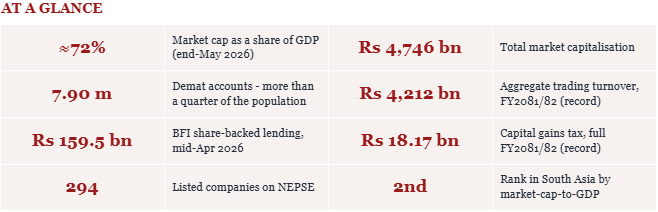

Nepal’s capital market has crossed a threshold that redefines its role in the national economy. Once viewed as a supplementary financial segment, the market has expanded in both size and reach to become a significant economic force. As of the end of May 2026, the total market capitalisation of companies listed on the Nepal Stock Exchange stands at approximately NPR 4,746 billion—equivalent to nearly 72 percent of the country’s GDP.

A market of scale and reach

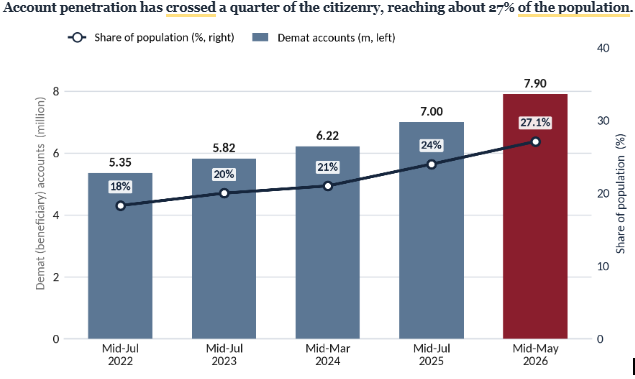

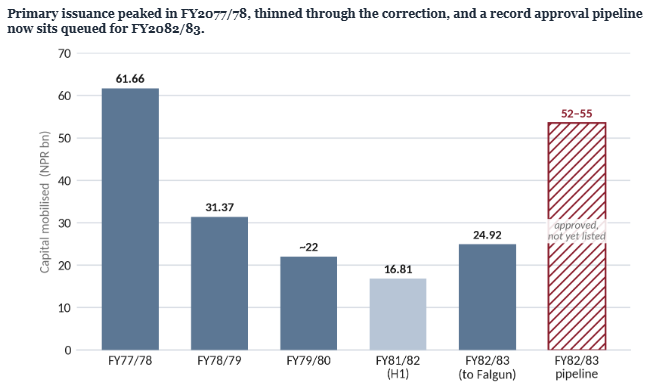

The growth trajectory of Nepal’s capital market reflects both recovery and structural expansion. Following a sharp correction, the market rebounded strongly, surpassing previous peaks in absolute value. Participation has also deepened significantly, with demat accounts reaching about 7.9 million—around 27 percent of the population.

This level of penetration is notable for a frontier market. More importantly, the participation pattern indicates a broad-based democratisation of investment, with significant inclusion of women and younger investors. However, while account ownership is widespread, active market participation remains lower, indicating a gap between access and engagement.

Structural depth vs valuation depth

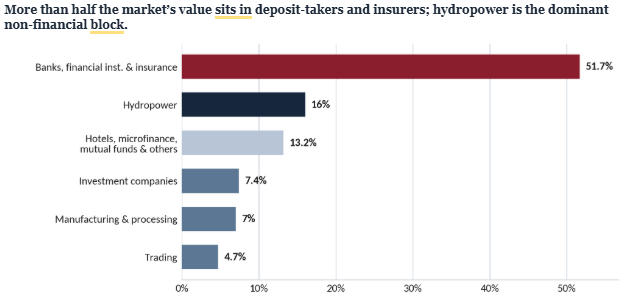

Despite its high market-cap-to-GDP ratio, Nepal’s capital market faces structural limitations. A large portion of shares remains locked in promoter holdings, leaving free-float capitalisation constrained. This limits liquidity and affects efficient price discovery.

The market is also heavily concentrated in the financial sector, where banks and insurance companies dominate total capitalisation. As a result, capital market performance is closely tied to the health of the financial system.

Integration with the banking system

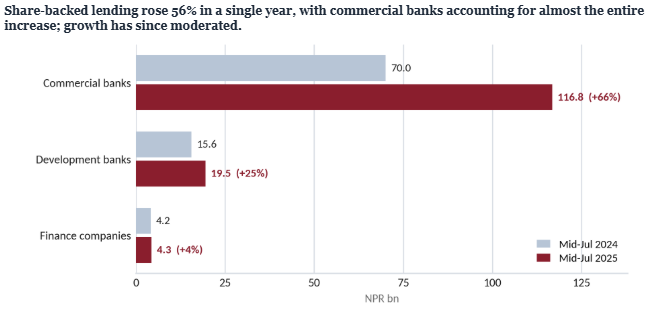

The capital market is deeply interconnected with the banking sector. Banks have extended substantial credit against shares, while market activities such as IPO subscriptions and trade settlements channel significant liquidity through the banking system.

This relationship introduces systemic implications. Market corrections can trigger margin calls and liquidity pressures, highlighting the importance of coordinated regulatory oversight.

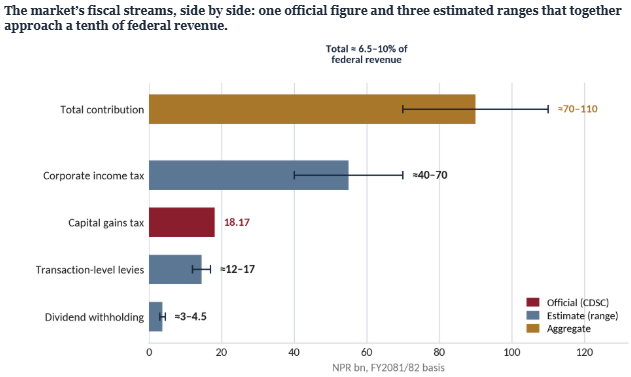

Fiscal Contribution and Economic Impact

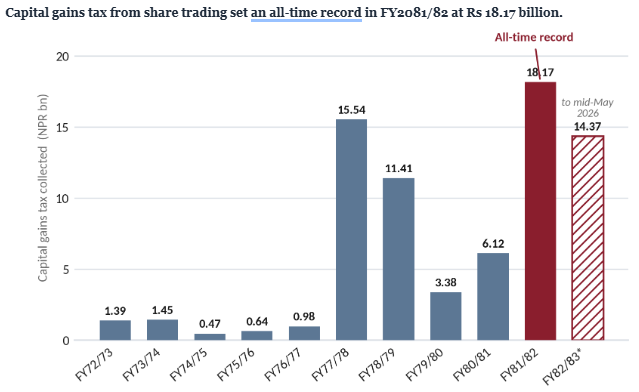

The capital market contributes meaningfully to public finances. Capital gains tax collections have reached record levels, complemented by transaction fees, dividend taxes, and corporate income tax from listed companies.

Beyond fiscal impact, the market also supports employment, financial inclusion, and capital formation. It has played a particularly important role in financing sectors such as hydropower, contributing to long-term development objectives.

Institutional capital: latent but underutilised

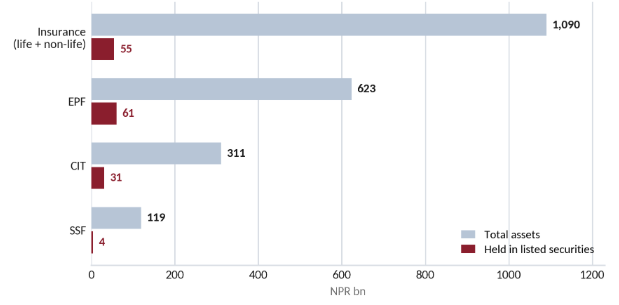

Nepal has substantial institutional capital in entities such as provident funds, investment trusts, and insurance companies. However, only a small portion of these funds is allocated to equities. This represents a major opportunity for market deepening.

Regional Standing and Structural Gaps

Nepal’s capital market ranks among the leading markets in South Asia in terms of market-cap-to-GDP ratio. However, structural gaps remain, including limited corporate bond markets, low institutional participation, and a narrow range of financial instruments.

Conclusion

Nepal’s capital market has decisively moved beyond the margins of the financial system to become a central pillar of the national economy. Its scale, reach, and interconnectedness now bind it directly to household wealth, banking-system stability, fiscal revenue, and long-term capital formation.

Yet, alongside this structural importance lies a critical institutional inconsistency. Despite being the regulatory body overseeing all listed companies—including banks and financial institutions—the Securities Board of Nepal (SEBON) continues to face recurring uncertainty around leadership appointments.

In contrast, the Nepal Rastra Bank operates with a clearly defined legal framework ensuring independence. SEBON, however, continues to be perceived as functioning in close alignment with the Ministry of Finance rather than as an independent regulator.

This inconsistency has broader implications for market confidence, regulatory continuity, and institutional credibility. A market of Nepal’s current scale requires a governance framework that reflects its systemic importance.

Aligning SEBON’s institutional independence with that of other key regulators is therefore essential. Strengthening regulatory autonomy will be critical to sustaining trust, ensuring stability, and supporting the continued evolution of Nepal’s capital market.

Adarsha Bazgain

Bazgain is deputy CEO of Nabil Bank.

Most Read from Columns

.png&w=300&height=200)

Editor's Picks

Nirmal Purja, who redrew the limits of human endurance and reshaped Nepali mountaineering, dies in Broad Peak avalanche

Habitat concerns grow as Nepal counts a record 429 tigers

The journey for fodder is too often becoming a final one

Built for adventure, held back by regulations

Bureaucracy gripped by fear and uncertainty as trust deficit deepens

E-PAPER | August 05, 2026

×