Inside the Rs 3.73 billion fraud investigation shaking Nepal’s business elite

How an informal alliance between a well-connected fixer and one of Nepal's oldest business families unravelled into a Rs 3.73 billion fraud investigation. Post Illustration

On a spring day in 2020, during the height of Nepal’s Covid-19 lockdown, police stopped a vehicle bearing diplomatic number plates and found 67 thermal guns inside. The devices, which sold for Rs 5,000 apiece, were allegedly being moved for resale at three times the price. The man in the vehicle was Sulav Agrawal, scion of the Shankar Group — one of Nepal’s oldest and most prominent business conglomerates — and, at the time, the country’s honorary consul general for Kyrgyzstan. He was arrested on the spot.

The arrest didn’t seriously damage the Shankar Group's business. But it shook its reputation, and more consequentially, it introduced the family to Deepak Bhatta — a well-connected businessman who, through a combination of political access and quiet influence, secured Agrawal’s release. For a family that had spent decades building commercial power without cultivating political cover, this was no small thing. They owed Bhatta.

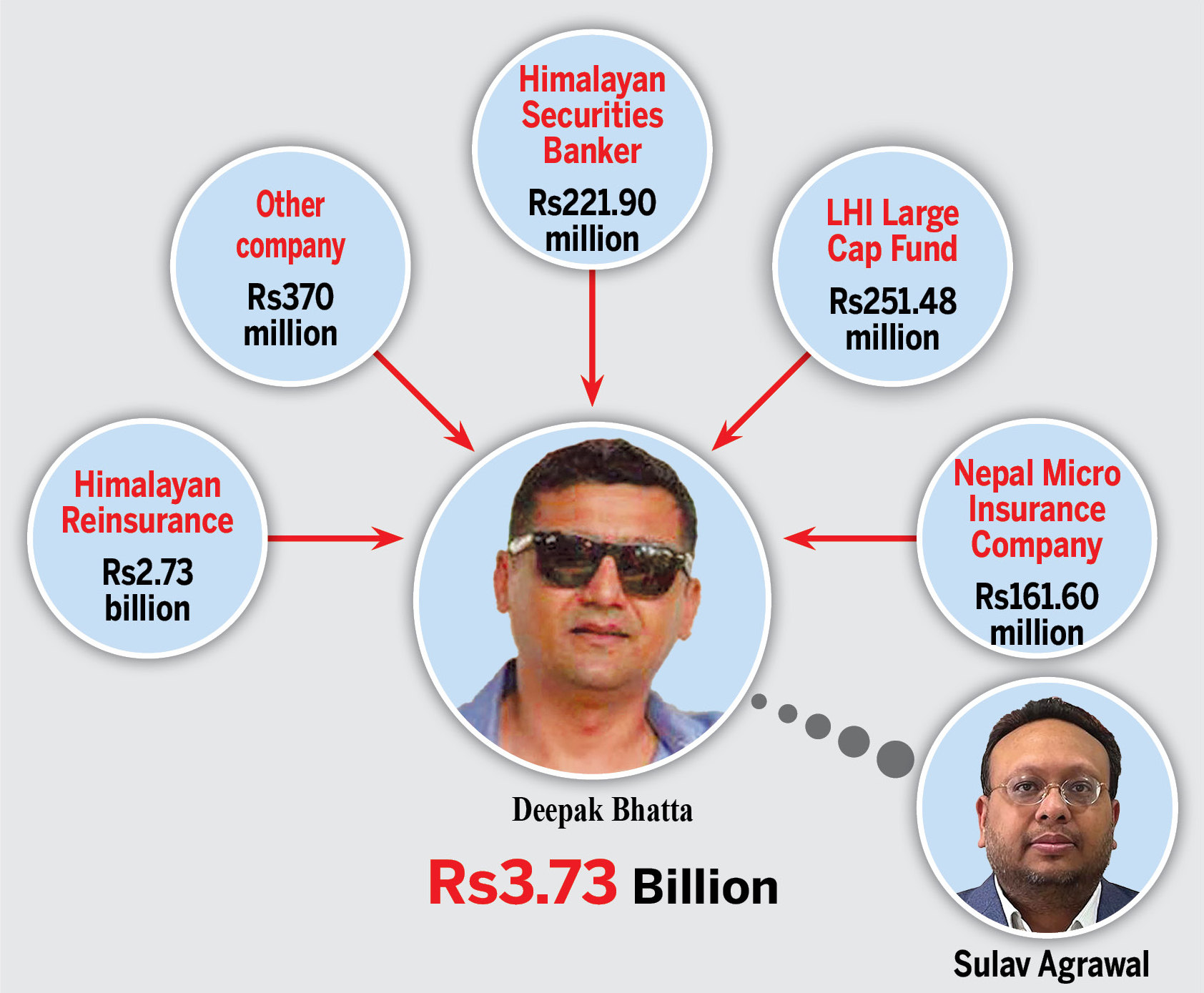

What grew from that debt — an informal, unwritten alliance between Bhatta and the Shankar Group — has now placed both at the centre of one of Nepal’s largest money laundering investigations. The Department of Money Laundering Investigation alleges that Bhatta illegally diverted approximately Rs 3.73 billion from five listed companies, including Himalayan Reinsurance, a firm the two parties built together, and used the proceeds to accumulate shares in a competitor. Several key figures are in custody. Bank accounts have been frozen. A case filing is expected within days. And a 91-year-old business empire is confronting the possibility that its most consequential partnership may prove to be its most damaging.

Kantipur spoke with ten people with direct knowledge of the matter, including officials at the Department of Money Laundering Investigation, two of the five partners at the centre of the agreement, sources close to Bhatta, Securities Board of Nepal, Nepal Stock Exchange, Insurance Authority, Nepal Rastra Bank and officials at Himalayan Reinsurance.

The immediate trigger for the investigation was mundane by comparison. Last July, at the start of the current fiscal year, five businessmen — Shekhar Golchha, chairman and managing director of Golchha Group; Rohit Gupta, vice chairman of Ramesh Corp; Rajbahadur Shah, managing director of Jawalakhel Group of Industries; Deepak Bhatta; and Amit More, managing director of Lucky Group — made an informal agreement to pool their money, deposit it into a shared bank account, and invest in Nepal’s stock market. The arrangement was neither unusual nor illegal. Funds were collected, wired into a single account through the banking system, and some shares were purchased. For a time, everything appeared to be proceeding as intended.

Except it wasn’t. When several partners began to notice irregularities, they demanded an explanation. What they found, according to one of the five businessmen who spoke to Kantipur, was that Bhatta had siphoned funds from the pool — and that the misappropriation ran far deeper than their shared account. Bhatta had allegedly used money belonging to the partnership, and to the five listed companies he was connected to (Himalayan Reinsurance, one subsidiary of Nepal Life Insurance, Himalayan Securities Banker, LHI Large Cap Fund, and Nepal Micro Insurance) to purchase large quantities of shares in the names of himself and Suvi Agrawal — wife of Sulav. The total purchase amount was Rs 3.73 billion. Nepal Life, in a statement on April 3, clarified that it has no link to the alleged share transaction involving Bhatta and Bhrikuti Stock Broking Company, broker number 55*.

“This has already been established through the Department’s preliminary investigation. They have also found evidence that all of this trading was conducted from Sulav’s office,” one of the sources who spoke told Kantipur. “Someone buys nearly Rs 4 billion worth of shares in your name and then claims he knew nothing about it — how is that believable? Every transaction sends an SMS to the account holder.”

Bhatta, in his statement to the Department, tells a different story entirely. He says he had a margin trading agreement with Bhrikuti Stock Broking Company, broker number 55, under which the firm would extend credit for share purchases, and accounts would be reconciled at year’s end. As part of that arrangement, he says in the statement, he handed over his trading platform login credentials to the broker. The purchases, he claims, were made without his knowledge.

“It appears that Sulav Agrawal obtained my credentials from the broker and used them to purchase large quantities of shares in my name and his wife’s name,” Bhatta stated. “I only found out 10 to 15 days ago. The broker and Sulav conspired — I was defrauded.”

He named Shahil Agrawal — Sulav’s brother, Managing Director of the Shankar Group, and chair of Himalayan Reinsurance’s Investment Committee — and Himalayan Reinsurance Chief Executive Officer Upasana Poudel as co-conspirators, alleging they liquidated Rs. 2.73 billion in shares held by Himalayan Reinsurance and funnelled the proceeds to the broker for Sulav’s use. Bhatta closed his statement with a request to be freed. He had been framed, he said, by his own associates.

But there is a foundational problem with this account. At the time the alleged margin agreement was in effect, no broker in Nepal had received regulatory authorisation to offer margin trading. The arrangement Bhatta describes as his alibi was itself against the law.

When Golchha, Shah, Gupta, and More confronted Bhatta at an emergency meeting last month, demanding the return of the misappropriated funds, it was already too late for a private resolution. Two sources who were at that emergency meeting told Kantipur that Bhatta lashed out at Sulav, who was profusely apologetic. “He said he was embarrassed, started weeping, and went on to touch Golchha’s feet to apologise,” the source said. The group discussed figuring out a way to repay the funds back to the accounts, but with a new government in power right after the Gen Z protests, regulators had already launched their probe. The bank accounts of both Bhatta and Sulav had been frozen right after the Gen Z protest, and remain frozen at the moment. The dispute between former partners had become a matter for the state.

Bhrikuti Stock Broking Company, the broker at the centre of the alleged scheme, has since been found by regulators to have committed three distinct violations. It collected no advance payment from Bhatta before executing trades, despite rules requiring brokers to collect at least 25 percent upfront. It used proceeds from Himalayan Reinsurance’s share sales to purchase shares in Bhatta’s name — a prohibited commingling of client funds that the Department’s investigation confirmed. And it extended open-ended informal credit to Bhatta rather than settling transactions within the mandatory three-business-day window, a practice the broker itself acknowledged in its regulatory filings.

NEPSE suspended Bhrikuti’s license indefinitely and referred the matter to the Securities Board, which has issued a show-cause notice. Himalayan Reinsurance has separately filed a lawsuit against Bhrikuti at the Kathmandu District Court, seeking recovery of the funds it says were never remitted.

The broker’s principal shareholder is Manoj Lal Karna, a former CEO of Himalayan Life Insurance, with the firm registered in his wife's name. Its CEO, Sandeep Chachan, is identified in Bhatta’s own statement as the central operational figure in the trades. Chachan is currently unreachable. Kantipur also tried to contact Shankar Agrawal and Shahil Agrawal of Shankar Group and Upasana Poudel multiple times through multiple channels, but did not receive a response.

The purpose behind the share accumulation, sources allege, was not merely financial. For months before the investigation began, Bhatta and his associates had been aggressively buying shares of Nepal Reinsurance Company — Himalayan Reinsurance’s principal competitor — on the secondary market. Nepal Reinsurance was preparing to issue rights shares, making early accumulation strategically valuable. Beyond that, sources say, the plan was either to absorb Nepal Reinsurance into Himalayan Reinsurance through a merger, or to so weaken it that Himalayan would dominate the market outright. What was framed as stock market investing was, in this reading, a corporate takeover strategy funded with other people’s money.

***

To understand the scale of what is alleged and why the Shankar Group is exposed, it is necessary to understand how deeply the two parties had become intertwined.

After Bhatta secured Sulav’s release in 2020, the partnership that developed was effective precisely because it was complementary. The Shankar Group, operating under the Jagdamba holding structure, had spent decades accumulating commercial weight — the group’s borrowings from banks and financial institutions alone exceed Rs. 30 billion. What it lacked was political reach. That’s where Bhatta came in. In return, the group’s capital and infrastructure gave Bhatta financial leverage he could not have assembled independently. When credit taken through their joint ventures is included, total outstanding borrowing across the partnership is estimated at close to Rs 100 billion, according to an official at Nepal Rastra Bank.

The insurance sector became their most significant joint project. Before 2014, Nepal had no domestic reinsurance company; premiums flowed abroad. When Nepal Reinsurance Company was established that year through a joint government-industry investment, the Shankar Group identified the sector as a priority. Sources allege that Bhatta engineered the appointment of former home secretary Surya Prasad Silwal as chairman of the Insurance Committee, with the explicit objective of securing reinsurance and micro-insurance licenses for the group. “Silwal delivered on both counts,” a source told Kantipur. In July 2021, Himalayan Reinsurance was established with paid-up capital of Rs. 10 billion, with the Shankar Group and Bhatta as its largest shareholders. (Editor’s Note: Kailash Sirohiya, chairman of Kantipur Media Group, is among several dozen early investors — alongside Nepal Bank Limited and Rastriya Banijya Bank — in Himalayan Reinsurance. Sirohiya purchased 1 percent share at face value for Rs 100 million.)

Sulav and Bhatta’s influence, sources allege, reached into government budget-making as well. A supplementary budget in fiscal year 2021/22 contained a tax exemption on sponge iron that benefited Jagdamba Steels while disadvantaging rival producers — a provision so narrowly drawn that several industrialists protested publicly. Then, on the eve of the 2022-23 annual budget, intermediaries were allegedly introduced into Singha Durbar overnight to adjust tax rates in favour of specific interest groups. Bhatta and the Shankar Group were named in connection with both episodes, and suspicious transactions were detected in their bank accounts around the same time.

Bhatta’s close aide, who spoke to Kantipur on condition of anonymity because he feared being scrutinised, defended some of the budget decisions. “Getting a tax exemption on sponge iron did not only benefit Jagdamba Steels, it also benefited dozens of other steel companies in the country,” he said. Bhatta himself has repeatedly defended the tax exemption in past interviews as being “good for the country.”

Nepal Rastra Bank’s Financial Intelligence Unit had already been watching. Examining transactions between Infinity Holdings and the Shankar Group from 2021 to 2023, the Financial Intelligence Unit (FIU) found that Rs 450 million had moved from a Jagdamba Steel account at Nepal Investment Bank into Bhatta's account at Siddhartha Bank. Jagdamba Steel’s own audit report for 2020/21 confirmed the transaction. The FIU further found that Rs 300 million was deposited into Bhatta’s overdraft account in mid-2021 and that Rs 450 million was subsequently withdrawn. The origin of that capital had never been satisfactorily explained.

The fallout has been swift and personal. Shekhar Golchha resigned as chairman of Himalayan Reinsurance the day he learned of the transactions. “None of this ever came before the board as a formal agenda item,” he told Kantipur in a phone interview. “The day I found out, I resigned.” He denied any personal benefit from the trades. Several other directors have privately acknowledged the irregularities.

With Bhatta and Sulav in custody, the Department has taken statements from Golchha, Shah, Gupta, More, and others. Their accounts, sources told Kantipur, consistently identify Bhatta and Sulav as the architects of the scheme. Evidence collection from the Rastra Bank, Securities Board, Insurance Authority, Nepal Stock Exchange, and CDS and Clearing Limited is complete. A case filing is expected imminently.

The thermal gun arrest that cost Sulav his freedom for a few days sparked this partnership six years ago. What the partnership built — and then destroyed — may cost far more.

*The story has been updated to incorporate clarification by Nepal Life Insurance.

21.03°C Kathmandu

21.03°C Kathmandu